PreSale Pitfalls: What to Know Before Buying a Condo OffPlan

HOME BUYERS – To get the best exclusive listings visit www.vreg.ca and go to “EXCLUSIVE DEALS”

Buying a condo before it’s built—often called buying “off-plan” or “pre-sale”—can seem like a smart move. Early access, lower prices, and VIP incentives are all part of the allure. But for many buyers, what starts as an exciting opportunity ends in costly frustration.

Before you sign on the dotted line, here’s what you need to know.

1. Construction Delays Are the Rule—Not the Exception

That “anticipated completion date” on the brochure? Treat it as a guess, not a guarantee. Developers often face delays due to labor shortages, permitting issues, supply chain bottlenecks, or weather disruptions. Contracts usually allow for extensions, sometimes for years. If your life plans hinge on that closing date—renting out your home, relocating, or locking in financing—you could be in trouble.

Protect yourself by negotiating a firm outside completion date and understanding your rights if the project is delayed beyond that window.

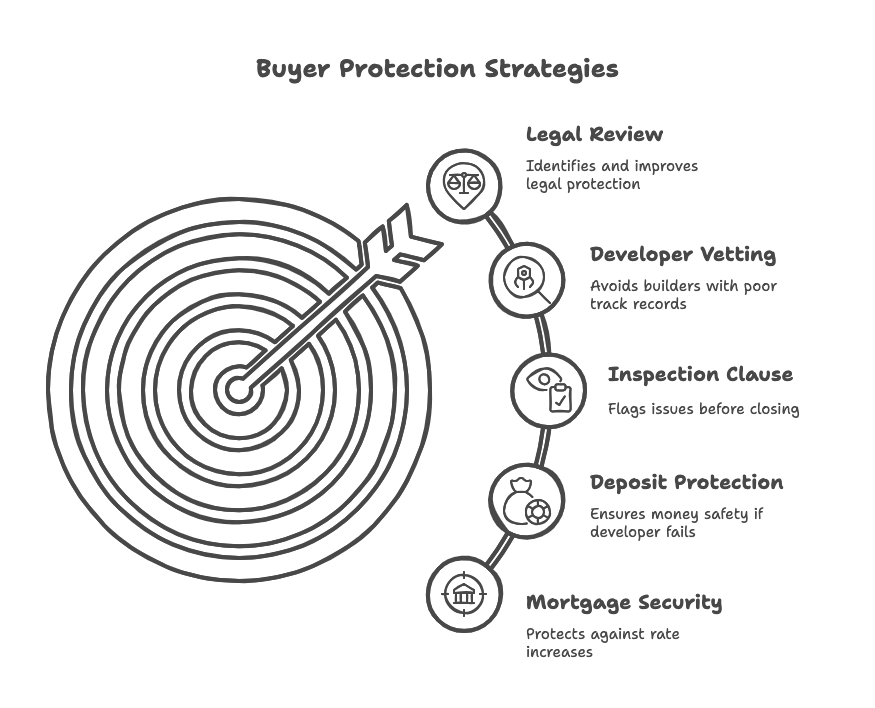

2. Financing Isn’t Guaranteed

You won’t get a mortgage today for a home that doesn’t exist yet. Most lenders issue final approvals within 90–120 days of completion, not years in advance. Between now and then, your financial situation, credit score, or interest rates could change—affecting your ability to qualify. In a declining market, even the appraised value could come in lower than your contract price, leaving you short on funding.

Smart buyers stress-test their finances, secure long rate holds if possible, and build in a financing condition if the developer allows it.

3. Your Deposit May Be at Risk

Pre-construction deposits are typically 5%–20% of the purchase price and can be tied up for years. If your financing falls through or you can’t close, you could lose that money. Even worse, if the developer cancels the project, you might face delays getting your deposit back—or lose interest income on those funds.

Always ensure your deposit is held in trust or protected by deposit insurance. And be crystal clear on the terms under which it’s refundable.

4. The Market May Shift Beneath You

Pre-sales lock you into today’s pricing. But the real estate market—and your personal finances—can change dramatically before you ever take possession. If prices fall or interest rates spike, you may regret locking in that number. Worse, if you planned to flip the unit, shrinking demand or oversupply could derail your exit strategy.

This isn’t a problem if you’re buying to live. But if you’re banking on appreciation, understand the gamble you’re taking.

5. Not All Developers Are Created Equal

A glossy presentation doesn’t guarantee execution. Some developers have a history of late completions, poor workmanship, or walking away from projects entirely. If your builder cuts corners or fails to deliver on what was promised, your options may be limited—and expensive.

Research their track record. Visit past projects. Ask about their warranty coverage. And avoid builders without a long, successful completion history.

6. What You See Isn’t Always What You Get

Floorplans can change. Windows get smaller. Ceilings get lower. The high-end appliances in the showroom suite might be swapped for cheaper models by move-in. Unless your contract includes specific specs, you could end up with something very different than what you thought you bought.

Push for detailed finish schedules and insist on the right to inspect your unit before final closing.

7. The Contract Isn’t on Your Side

Pre-sale agreements are written by the developer’s legal team—and they’re not there to protect you. These contracts often include “sunset clauses” that allow the builder to cancel the deal if construction isn’t completed by a certain date, without penalty. Other clauses allow design changes, material substitutions, and possession delays.

Hire an experienced real estate lawyer to review every word. It’s not just about what’s in the contract—it’s about what’s missing.

Final Thoughts

Buying a pre-sale condo isn’t wrong—it’s just risky. If you understand those risks and structure the deal carefully, it can still be a smart move. But go in eyes open. Don’t let the showroom dazzle distract you from the fine print. The more you prepare, the better your chances of turning that empty blueprint into a solid financial win.